Phoenix’s divergence suggests more resilient local fundamentals—migration, job growth, and supply constraints. Nationally, median home prices were down ~0.6 % and pending sales were collapsing ~31 %, indicating broader weakness. The relative strength tempers downside risk in Phoenix-centric holdings. From tax revenue projections, this resilience helps sustain municipal forecasts. Policymakers may point to this in justifying infrastructure or housing policy. For value stability, the local cushion provides greater breathing room than many other U.S. markets.

Teravalis, a 33,800-acre development in Buckeye, envisions up to 100,000 homes and 55 million sq ft of commercial development but has only secured water for its first ~8,500 lots. State groundwater restrictions have paused approvals for many subdivisions. The stress underscores that future growth is increasingly tied to water allocations, regulatory approvals, and negotiations with tribal or utility authorities. For developers, water risk is now a core underwriting line. From a tax perspective, delayed buildout slows projected revenue. Regulatory frameworks may tighten further, and sustainable water innovations (reuse, desalination, leasing) become central for project viability.

Olea Scottsdale is being developed north of Loop 101 and east of Scottsdale Road, with careful setbacks (25 ft along main roads, 75 ft for townhouses) and desert landscaping buffers. The project is slated for phased completion through 2027. It targets high amenity, middensity multifamily + attached product in a premium suburban submarket. For real-estate investors, the scale and location may provide yield plus appreciation potential. Local jurisdictions will monitor infrastructure demand (roads, utilities) and traffic impact. The addition helps meet Scottsdale’s multifamily supply needs while aligning with sustainable growth patterns.

Slated to break ground by late 2025 with a ~36-month construction timeline, Astra Phoenix will redefine the downtown skyline. Its mixed-use program (vertical stacking of commercial, residential, hospitality) promotes densification. From a portfolio perspective, premium vertical product in central cores often commands better rent and stability. Zoning and permitting risk is substantive for such scale; incentives or height overrides might be required. For tax and municipal planning, increased density yields more property tax and systems demand. Its design likely will incorporate green systems given current best practices.

The projects address demand spillover from central Phoenix to peripheral areas such as Maricopa. The Sanctuary master plan is one of the larger new proposals south of the metro. These add supply but also stress infrastructure, utility extension, and water sourcing. Investment risk is higher in fringe zones due to longer absorption times and infrastructure cost. From a tax vantage, these areas may require public subsidies or impact fee structuring. Regulatory approvals (entitlements, grading, environmental) will be bottlenecks. In terms of long-term stability, communities closer to major arterials or transit corridors may outperform in such growth zones.

The Valley is seeing many sellers withdraw properties rather than reduce price or continue listing, driven by mismatches between seller expectations and buyer demand. Heat, mortgage rates, and buyer caution all factor. This trend increases illiquidity risk for residential portfolios. From a tax perspective, fewer closed sales slow turnover and thus compress transaction tax revenue. Local governments may respond with incentive or marketing programs. In value terms, homes in prime nodes or strong school districts will better resist these pressures.

The acquisition includes retail, office, and experiential components. The improvement plan emphasizes infrastructure upgrades, curated tenant mix, and experiential retail elements. Phased work is timed to minimize disruption. Such repositioning deals often reveal value-creation opportunities in undercapitalized assets. For investors, this is a signal that well-located assets still attract capital even amid softening market conditions. Local tax capture or improvement district structures may be involved. As for sustainability, renovations often incorporate energy retrofits, waste reduction, and modernized systems.

In recent weeks, Phoenix has seen its number of active listings rise markedly compared to prior quarters; concurrently, about 5.5 % of listings in a given week are undergoing price cuts. This dynamic signals softening seller leverage, particularly outside top-tier neighborhoods. For wealth holders, this underscores the need for granular underwriting. Municipal tax bases may feel pressure if downward adjustment persists. Regulators may reconsider permit timing incentives or relief. From a resilience lens, established, amenity-rich areas will remain comparatively stable.

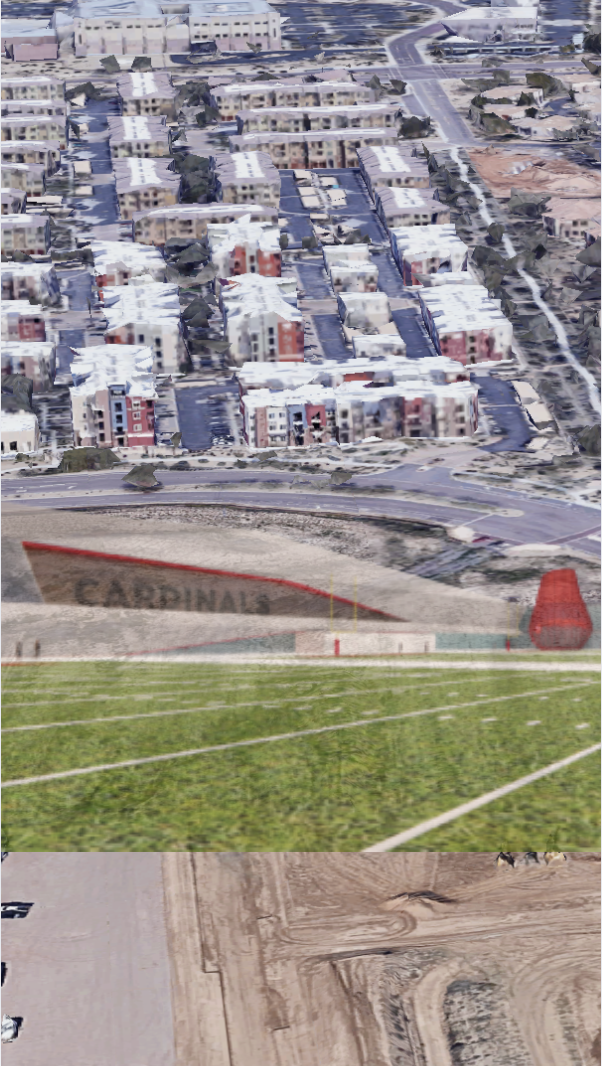

Arizona Cardinals’ $136 Million “Headquarters Alley” Project: How a 217-Acre Deal Will Redefine North Phoenix by 2028

Arizona Cardinals’ $136 Million “Headquarters Alley” Project: How a 217-Acre Deal Will Redefine North Phoenix by 2028 Public Safety as an Asset Class: The New Scottsdale AdvantageIn today’s Smart City economy, safety isn’t simply about peace of mind—it’s becoming a measurable, marketable asset class. Scottsdale is proving that public safety can be engineered into the fabric of

Public Safety as an Asset Class: The New Scottsdale AdvantageIn today’s Smart City economy, safety isn’t simply about peace of mind—it’s becoming a measurable, marketable asset class. Scottsdale is proving that public safety can be engineered into the fabric of

Nice to meet you! I’m Katrina Golikova, and I believe you landed here for a reason.

I help my clients to reach their real estate goals through thriving creative solutions and love to share my knowledge.